Please note: this report is very old to the point where it is useless. You must not consider it to be current. Many things may have changed, and it may well be that I no longer believe this company to be an attractive option. Please consider it an archive only.

It’s no secret that the ageing population will result in gradually increasing expenditure on healthcare for the next 3 decades. However, it’s relatively rare to find a company that is exposed to these trends, already pays a decent dividend, and is not exorbitantly priced. LifeHealthcare Group Ltd (ASX:LHC), which listed about 9 months ago, appears to be one such company.

I bought a some shares of the company at $2.33, just prior to the ex-dividend date, which was 3 September 2014. I wanted to wait until I'd spoken to management before writing about it, although that was more than a week ago now. The price is now $2.42, which, taking into account the dividend , is effectively 7% higher. It kinda got away from me there. What can you do?

On a lighter note, I did speak to the CFO David Wiggins who treated me with kindness and gruffness with lashings of respect. I think this is a good sign. We didn't speak for long, but he passed my basic interview test which is - can you talk about everything I don't like about your business without being rude to me? You would be surprised at how many companies' management cannot pass that test, and indeed I sold down another position recently for that exact reason. But I diverge...

What is the business of LifeHealthcare Group?

LifeHealthcare is in the business of distributing medical devices such as the robotic systems used for spinal surgery as well as the plates that surgeons implant to hold spine grafts in place. The company has historically grown by acquisition and is likely to continue on that path.

Shareholders are likely to benefit from private-public arbitrage, that is, the fact that the company can acquire smaller unlisted businesses at a discount to the going rate for a similar publicly listed company. On top of that, operating expenses can be stripped out of acquired companies.

The company is right to expand into hip and knee replacement devices and coronary stents, because demand for these devices is extremely sensitive to the ageing population. The simple fact is that the elderly are more likely to need a hip or knee replacement after a fall, or a coronary stent after a heart attack. Demand for these products is sure to grow steadily – the challenge for LifeHealthcare is to capture some of that market.

Although the business is not particularly exciting, the fact that it already distributes around 50 different products means that its fortunes do not depend on the popularity of any one product. Indeed, as the company offers new products, it becomes a more defensive investment because its revenue streams become increasingly diverse.

Who is running the show?

The CEO Daren McKennay founded the company and still owns about 3.4% of the shares, despite divesting some in the IPO.

According to the CFO David Wiggins, who also has a meaningful shareholding, LifeHealthcare has “focussed on moving into high-end device product areas” over the last 6 years. This is important because the company has more pricing power with high-end, clinically differentiated, products. Put simply, surgeons will encourage patients to pay more for top-of-the-line implants, and prefer to use the best equipment when operating.

The acquisition strategy is to focus on expanding existing clinical channels. For example, the company already supplies cardiac ultrasounds to heart surgeons, and will use existing relationships to market implantable coronary stents. Similarly, the company will leverage its existing repair and replacement sales channel to expand into primary implants.

What are the main risks?

As an importer, the company will have to increase prices if it is to maintain margins as the Australian Dollar weakens. In any event, a high Australian dollar benefits this company, and a weak Australian dollar hurts it. Although the company uses hedging to smooth the impact of currency fluctuations, if it turned out the company has insufficient pricing power to adapt to a lower Australian dollar, that would hurt the thesis.

An inflationary environment would also hurt the company, which has to fund inventory and is rather capital intensive. This is not a business with what I call "good economics." However, because it is planning to expand into hip and knee replacement, there is a good chance that this ugly duckling can turn into a swan. If not, well, ducks can be pretty beautiful if well looked after.

The other main risk is that the company pursues earnings growth even at unattractive rates of return. It is therefore important to monitor any acquisitions, especially while the balance sheet carries debt, because management is incentivised to grow earnings per share, rather than to achieve a high return on capital invested. I would view a significant increase of debt unfavourably, and I would get really annoyed if they paid more than 7 times EV/EBITDA for an acquisition. I'd also get really annoyed if they acquired a distributor that didn't have clinically differentiated (and sometimes superior) products.

Shall we look at some numbers?

LifeHealthcare is targeting a dividend payout ratio of 50–70% of statutory NPATA subject to working capital and capital expenditure funding requirements. NPATA was $7.5 million in FY 2014. Assuming that figure remains flat (a conservative assumption in my opinion), then the forecast dividend yield for FY 2015 is 3.5 - 5% only partially franked. However, I would consider the likely total dividend yield at the current price to be in the vicinity of 5 - 6%, partially franked, likely to grow.

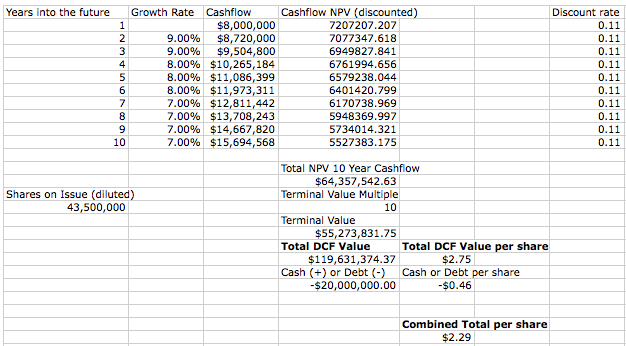

In recognition of the fact that my discounted cashflow valuations are a black-box that no-one understands, I'll show you a more traditional DCF valuation for LifeHealthcare. However, please note that that this is one of about 20 valuations I did with different inputs. My use of discounted cash-flow valuations is in order to apply the Pabrai philosophy of heads, I win, tails I don't lose much. The big winning part for LifeHealthcare that as a business it should last more than 10 years. It's not the best investment I've ever made, but I considered it worthy of a position in my portfolio at an effective price of $2.26 per share.

The reason I've predicted so much growth in cashflow is because I think that growth in receivables ($3 million) was higher than usual compared to growth in payables ($1 million). Although, sadly, I'd expect receivables to grow over time in a business with poor economics such as device distribution, the fact that profit was higher in 2014 than 2015, but cashflow was higher in 2013 than 2014, suggests that the balance sheet movements had an impact. I've made some allowance for the ever-necessary capital expenditure, but have I allowed enough? I'm out on a limb because of this company's lack of history as a listed company.

What this DCF model proves, one way or another, is that the company is not cheap (by my fairly harsh standards) unless it makes some good acquisitions.

My reasoning is that the company has been built on acquisitions so far, and while we shareholders wait for them to do another good acquisition, we are paid a decent dividend. If the company does not make a good acquisition, then at least debt should be reduced a bit and so, therefore will risk. I am not overly excited about investing in a business that is not inflation resistant, but I am willing to give management a chance to show they have enough discipline to stick to the kind of "business channels" where they can maintain pricing power. I'm willing to wait and see if they can pay the right price for the right businesses. I see value at $2.40, and I stand by my decision to buy at an effective price of $2.26, though the impact of a falling currency concerns me.

It all comes down to faith in management.

The author owns shares in LifeHealthcare. The purpose of this blog is to document my thoughts on different companies in an easily accessible way and to make connections with likeminded investors. Subscribers to the Free Newsletter get sent research first, and have access to the Hidden Research.

Getting to be good value at the current price of $2.27. If the AUD drop really sets in it could get interesting - definitely hurts profits. Having said that, that could create a decent environment for the right kind of acquisition.

Link

I took a look at this company almost 6 months ago. My big worry is definitely the economics of the business model of the company. LHC seems like a middle man, without the power to raise prices or affect demand. While the play on the ageing population theme is attractive by getting into the hip replacement business, I still don't feel comfortable about the business. Perhaps if it's far cheaper, I may consider it (say around the $2 mark).

LinkOne of the main competitive advantages (and threats) for LifeHealthcare is its army of sales people. These are no ordinary run of the mill sales people. They are highly trained and guide surgeons on how to use the products they distribute, even sitting in on operations. So these are not simple products an Ebayer could import and then sell at a cheaper price.

LinkAs Claude says one of the main ways this company can grow is through acquisitions - i.e. buying more highly skilled sales people in different products in effect.

Cheers

Mike

Disclosure: I own shares in LifeHealthcare.

Thanks for contributing Mike - much appreciated. I think that's something I probably underplayed in the above analysis. The falling Australian dollar isn't great for the company, but I do think the business quality is much higher than the average importer - and that competitive advantage is important.

LinkYes I share your concerns, as it is not the best value play I've ever seen. Having said that I think that it will either be a decent income stock or a decent growth stock - and one I'm willing to give enough rope to see if they can make some good acquisitions.

LinkThanks for commenting Paul!