Introducing Clinuvel: A New Ethical Equity For September

Clinuvel Pharmaceuticals (ASX:CUV) is a profitable and growing biopharma company. Its drug, SCENESSE (afamelanotide 16mg), is used to treat erythropoietic protoporphyria (EPP), a rare genetic disease characterised by severe intolerance of the skin to light. SCENESSE is approved in Europe and is in the final stages of gaining marketing access in the US. I believe the stock represents good value based purely on the potential for SCENESSE in Europe. US approval would double the addressable market for SCENESSE and Clinuvel has a pipeline of other compounds and indications.

Clinuvel Background Information

The scientific basis of SCENESSE originated at the University of Arizona Cancer Centre in 1987 with the development of a synthetic hormone designed to protect the skin. Clinuvel (or EpiTan as it was called then) acquired the technology and listed on the ASX in January 2001 with the aim of developing a tanning product, Melanotan.

Current CEO, Philippe Wolgen, took the helm in 2005 and the board appointed the late Dr Helmer Agersborg as Chief Scientific Officer (CSO) at the same time. The pair switched the company’s focus towards addressing light-related skin disorders including EPP. The main accomplishment of the company to this point was to develop a sustained release delivery mechanism, improving both efficacy and reducing side effects.

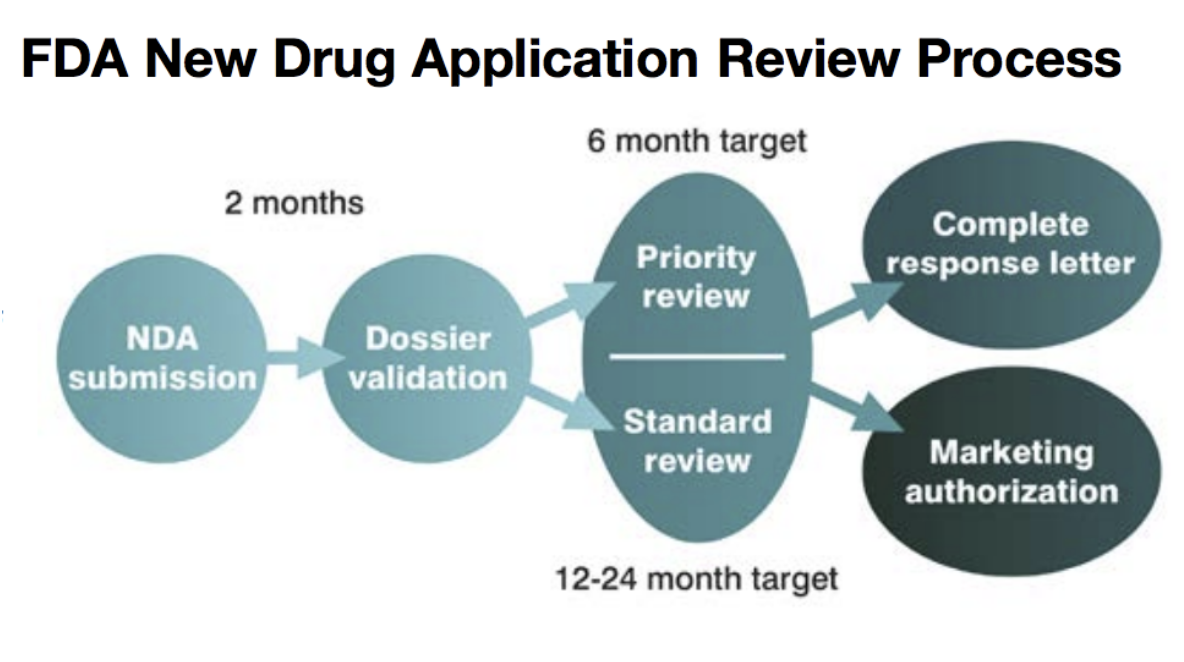

In 2010, afamelanotide was added to the list of drugs reimbursable by the Italian National Health System for EPP and in 2012 two leading Swiss insurers agreed to reimburse the drug. Clinuvel finally received full European approval in 2014 following the longest ever regulatory review by the European Medicines Authority (EMA). In June 2016, the first EPP patients received the drug under the approval. A New Drug Application (NDA) was submitted to the US Food and Drug Administration (FDA) in June 2018.

Clinuvel Intellectual Property

SCENESSE

SCENESSE, or afamelanotide, is a synthetic version of the alpha-melanocyte stimulating hormone (α-MSH) which naturally occurs in the body. Skin cells release α-MSH when subjected to ultraviolet radiation (UVR). Once released, the half-life of α-MSH is a few seconds, which is sufficient time to reach and stimulate other skin cells called melanocytes which then produce melanin. Melanin is a dark brown pigment which causes tanning and protects the skin from sunlight.

SCENESSE differs from α-MSH in that it is 10 - 1,000 times more potent and has a half-life of 30 minutes. The drug is further enhanced by Clinuvel’s patented controlled release delivery mechanism which involves injecting an implant about the size of a grain of rice under the skin. This doubles melanin density levels and reduces side effects compared to daily liquid injections of afamelanotide. The effects of a single implant last around two months.

Side effects of SCENESSE include nausea and headaches which may be experienced by more than 10% of people. Diarrhoea and vomiting, abdominal pain, drowsiness and decreased appetite may affect up to 10% of people.

EPP

EPP is a genetic disease which is estimated to affect between 1 in 75,000 and 1 in 200,000 people and is more prevalent in fair skinned people. Sufferers do not produce sufficient ferrochelatase, an enzyme which converts protoporphyrin IX into heme B. Consequently, abnormally high levels of protoporphyrin IX accumulates in the blood and skin. Protoporphyrin IX undergoes a chemical reaction when exposed to sunlight which causes severe pain, swelling and scarring of the skin. Many EPP sufferers avoid the sun altogether, including light from windows, with severe psychological consequences.

SCENESSE is the only approved drug for treating EPP and is currently only approved in Europe. Over two decades, more than 1,400 patients have received more than 4,500 doses of the drug in clinical trials and post approval. Clinuvel closely monitors the safety profile of SCENESSE in order to maintain marketing permission for the therapy from the EMA. More than 95% of patients treated with SCENESSE continue treatment beyond the first year and some in Switzerland have been receiving treatment for more than a decade. The drug works and has proven to be safe up to this point, so US approval is a real possibility.

Clinuvel’s development pipeline includes a paediatric (for children) formulation of SCENESSE for EPP.

Vitiligo

Vitiligo is a more common disease than EPP affecting between 0.1% and 2% of people and is a second potential indication for SCENESSE. The cause of vitiligo is unknown and the disease is characterised by patches of skin losing their pigment. It is more noticeable in people with dark skin and can cause sufferers to be stigmatised. One of the main treatments currently available is UVB therapy, where patients are exposed to controlled quantities of UVB light.

Clinuvel has undertaken two Phase II clinical studies of SCENESSE in vitiligo.

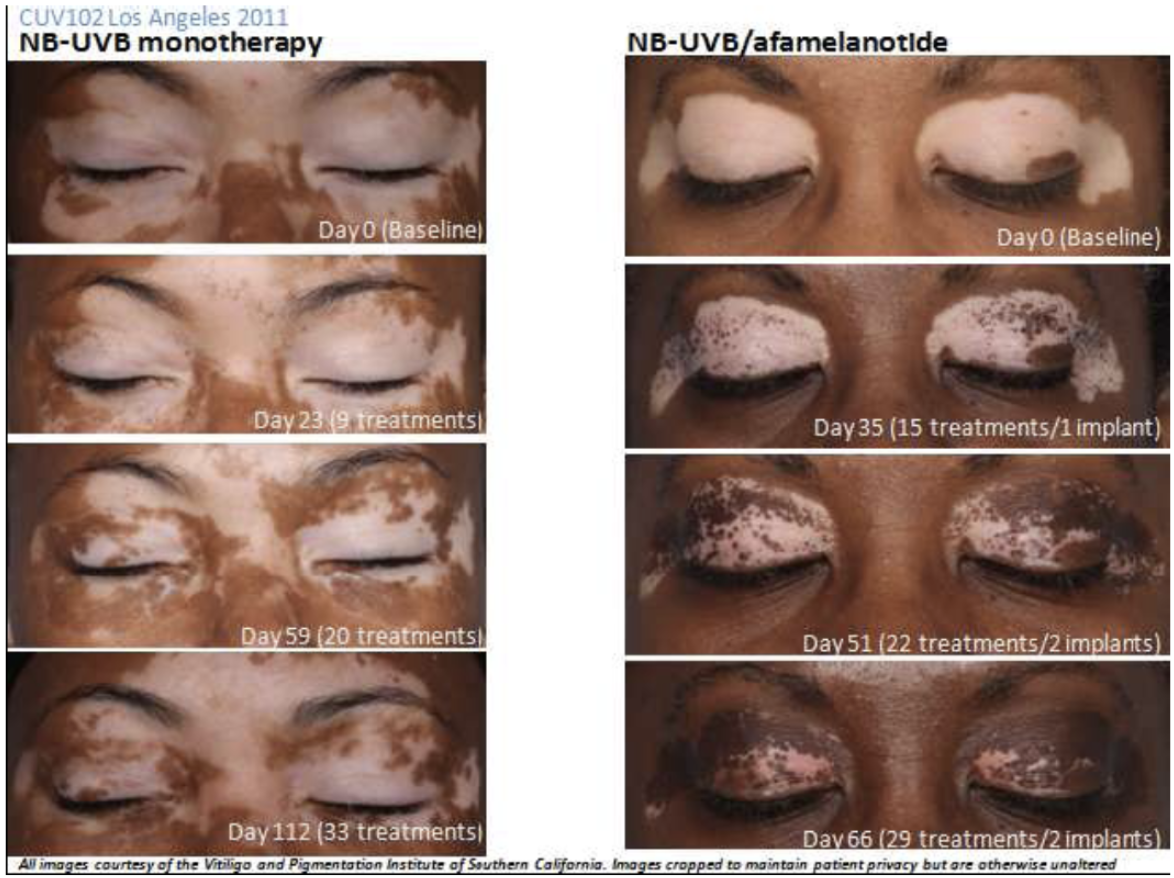

The first was an open-label study conducted in the US comparing SCENESSE plus UVB therapy against UVB therapy alone. 54 patients were enrolled with half assigned to each treatment arm. 41 patients completed the study and the extent of repigmentation in those receiving SCENESSE was significantly greater than observed in the control group. A follow up study showed that depigmentation did not reoccur in patients who received a combination of SCENESSE and UVB therapy.

Only 75.9% of patients completed the US Phase IIa study with 13 withdrawals, including five who failed to complete the study “due to the intensity of pigmentation experienced”. It would appear there is real potential, but with the possible drawback that the drug makes the unaffected skin darker.

A second double-blind (meaning that neither the patients nor those running the trial know which patients are receiving the drug) study is ongoing in Singapore that was initiated in May 2014. Promising preliminary results were released in December 2015 for the seven patients who had completed the study up to that point, with an additional patient withdrawing consent. A further 13 patients were enrolled under “an expanded open‐label protocol” with completion of treatment expected by February 2016, but Clinuvel is yet to publish these results.

A more rigorous vitiligo study is planned in the US following FDA approval for EPP.

The above images are of two different patients in the US Phase IIa study. Note the change in skin tone in the unaffected areas for the patient receiving the combination therapy.

The vitiligo progress seems encouraging but the following question remain unanswered:

The pilot Phase IIa trial in the US was originally supposed to be double the size with half the study conducted in Europe. What happened to the European part?

Why were only 8 patients initially enrolled into the Singapore study given the prevalence of vitiligo?

Why haven’t the final results from the Singapore trial, including the 13 additional patients, been released given the final treatments were completed in early 2016?

The five month follow up to the US study showed that depigmentation did not reoccur in those patients treated with the combination therapy. Does this mean that vitiligo sufferers would only require a single course of treatment if SCENESSE is approved? In comparison, EPP patients must receive the treatment on an ongoing basis.

Why did almost 25% of patients drop out of the US study?

Does SCENESSE further darken the dark parts of the skin as well as the light patches in vitiligo sufferers?

Topical Delivery

Clinuvel has been developing topical products in the background over the past couple of years under a joint venture with Biotech Lab Singapore, called Vallaurix. Early this year the company purchased the rest of Vallaurix and it is now a 100% owned subsidiary of Clinuvel. Two publicly disclosed products are under development, CUV9900 and VLRX001, and in a letter to investors in January 2018 chairman Stan Mcliesh stated that “Clinuvel will launch its premiere non-pharmaceutical product lines under private label”. It is unclear what the long-term strategy is here but perhaps it includes creating a topical version of SCENESSE to target light patches of skin in Vitiligo sufferers.

Recent Patents

Clinuvel holds patents for treating sufferers of central nervous system (CNS) disorders including Multiple Sclerosis (MS) and Alzheimer's Disease (AD) with α-MSH analogues (such as afamelanotide). It has also filed a patent in August 2018 for using α-MSH analogues to treat xeroderma pigmentosum (XP), a rare genetic disease where sufferers have a decreased ability to repair DNA damage. The company holds other patents for targeting inflammatory disease such as inflammatory bowel disease (IBD).

EDIT: The US patent for CNS disorders was rejected and others for inflammatory disease have not been issued either. Apologies for the initial oversight.

Scientists in Italy conducted a study published in 2015 indicating that afamelanotide induces cognitive recovery in Alzheimer transgenic mice. The authors suggested “MC4 receptor agonists (of which afamelanotide is one) could be innovative and safe candidates to counteract AD progression in humans”.

Clinuvel Competition

SCENESSE has been granted orphan status in both the US and Europe for treating EPP. Therefore, Clinuvel has exclusive marketing rights for seven years in the US and ten years in Europe post approval. SCENESSE was approved in 2014 in Europe and so exclusivity will expire in 2024.

SCENESSE is also protected by patents. These cover the controlled release delivery mechanism of SCENESSE and the use of alpha-MSH analogues to treat phototoxicity. The key patents were lodged in the 2000s so Clinuvel should remain free from competition in the XPP market at least until the late 2020s, unless another drug is developed.

Beyond that, it is possible that generics will emerge given Clinuvel currently earns between €56,000 and €85,000 per patient per year for SCENESSE. Clinuvel is required to monitor safety and prevent off-label use to retain marketing approval in Europe and this may provide a barrier to entry. Another could be the difficulty in achieving clinical equivalence given the complex delivery method of SCENESSE.

I have come across two companies besides Clinuvel that are actively developing Melanocortin 4 (MC4) receptor agonist drug candidates, Palatin Technologies and Rhythm Pharmaceuticals.

Palatin is developing Bremelanotide to help restore sexual desire in premenopausal women with hypoactive sexual desire disorder (HSDD) and has completed Phase III trials. The drug is very similar to afamelanotide and, like afamelanotide, originated in the University of Arizona.

A researcher at the University of Arizona accidently discovered the potential for MC4 receptor agonists to treat sexual dysfunction while developing the tanning drug, melanotan-II, that Clinuvel later acquired. He mistakenly self-administered twice the dose of melanotan-II that he intended and experienced an eight hour erection, nausea and vomiting!

Rhythm Pharmaceuticals is developing setmelanotide to treat genetic causes of obesity and has completed Phase II trials in two indications.

Clinuvel Market Potential

Between 1 in 75,000 and 1 in 200,000 people suffer from EPP and the disease is more prevalent in those with fairer skin. SCENESSE is priced at between €56,000 and €85,000 per patient per year and currently the recommended maximum number of treatments per year is four. Each treatment lasts for two months so the maximum revenue each patient could generate is €120,000 per year, assuming a treatment costs around €20,000.

Orphan drugs are usually more expensive than non-orphan drugs but SCENESSE seems pricey even for an orphan drug. A European study done in 2011 found that annual prices for orphan drugs ranged between €1,251 and €407,631 with a median cost of €32,242.

The UK National Institute for Health and Care Excellence (NICE), which decides which drugs are made available under the National Health Service (NHS) seems to agree. It has decided not to recommend SCENESSE as it did not meet its health-economic criteria. Clinuvel plans to appeal the decision but given the company has a uniform global pricing policy, it is quite possible that no agreement will be reached.

Although SCENESSE is costly for payers, I think it is important to recognise that orphan drugs need to command high prices in order to attract capital to develop them in the first place. This is because of the following reasons.

By definition orphan diseases affect a small number of people and so represent a small market opportunity for drug companies if prices are low.

High prices are temporary in most cases as exclusivity and patents only last a set number of years after which generics can enter the market.

The chances of getting a drug approved are low (less than 10% according to some statistics). The returns generated by individual companies need to be viewed in the context of the industry as a whole.

Drug development is not cheap. Clinuvel has raised $150 million in external capital to date.

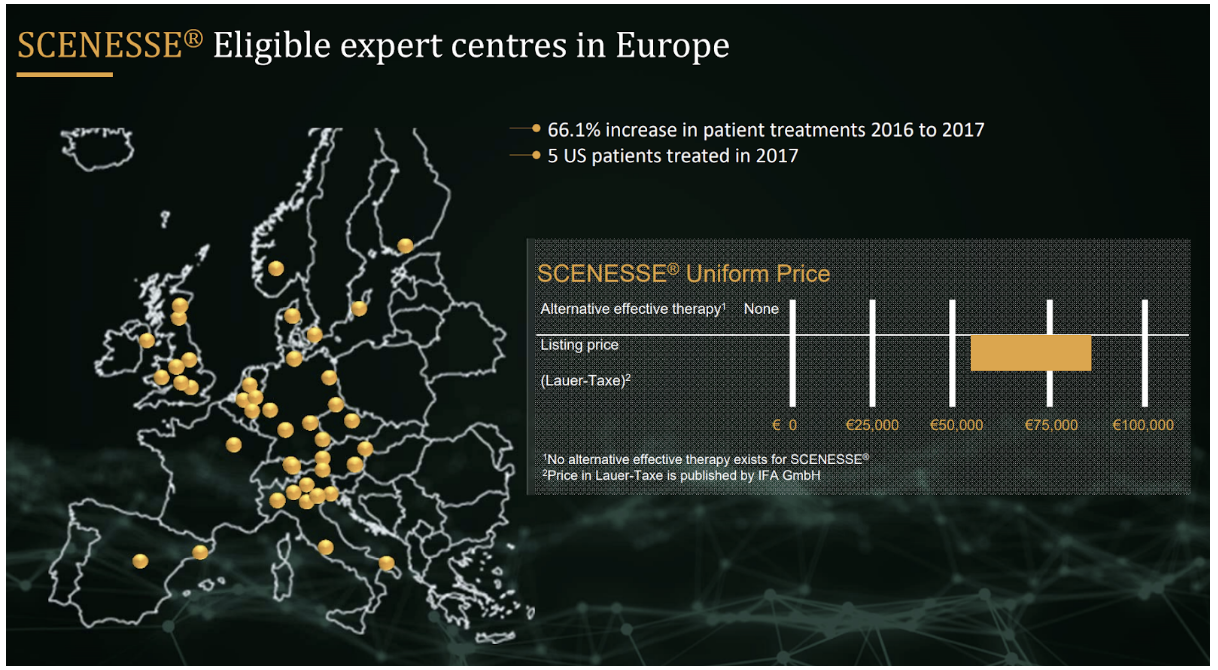

Clinuvel successfully negotiated pricing with the German National Association of Statutory Health Insurance Funds (GKV-SV) in 2017. Including Germany, patients have been treated with SCENESSE in six EU countries plus Switzerland.

There are 328 million people living in the following European countries: Finland, Ireland, Norway, Germany, Sweden, Belgium, Switzerland, Italy, Netherlands, Austria, Spain and France. These are wealthy countries and there is a good chance that EPP sufferers living in them will have access to SCENESSE. The majority of these nations also have high populations of fair skinned people who are more likely to suffer from EPP. Assuming the lower end of both the prevalence range for EPP and price range for SCENESSE, these countries represent a $150 million revenue opportunity. The opportunity could be as much as $600 million assuming the high end of the ranges. Including the UK, the figures are $180 million and $721 million respectively.

US approval could be up to 24 months away but may happen much sooner if SCENESSE receives a priority review. The decision will be made after Clinuvel has provided additional documents requested by the FDA. The US effectively doubles the addressable market for SCENESSE.

The total revenue opportunity for EPP is between $330 million and $1.32 billion assuming UK reimbursement, FDA approval and consistent pricing,. The market for Vitiligo is bigger than EPP should Clinuvel achieve FDA and EMA approval.

Clinuvel Financials

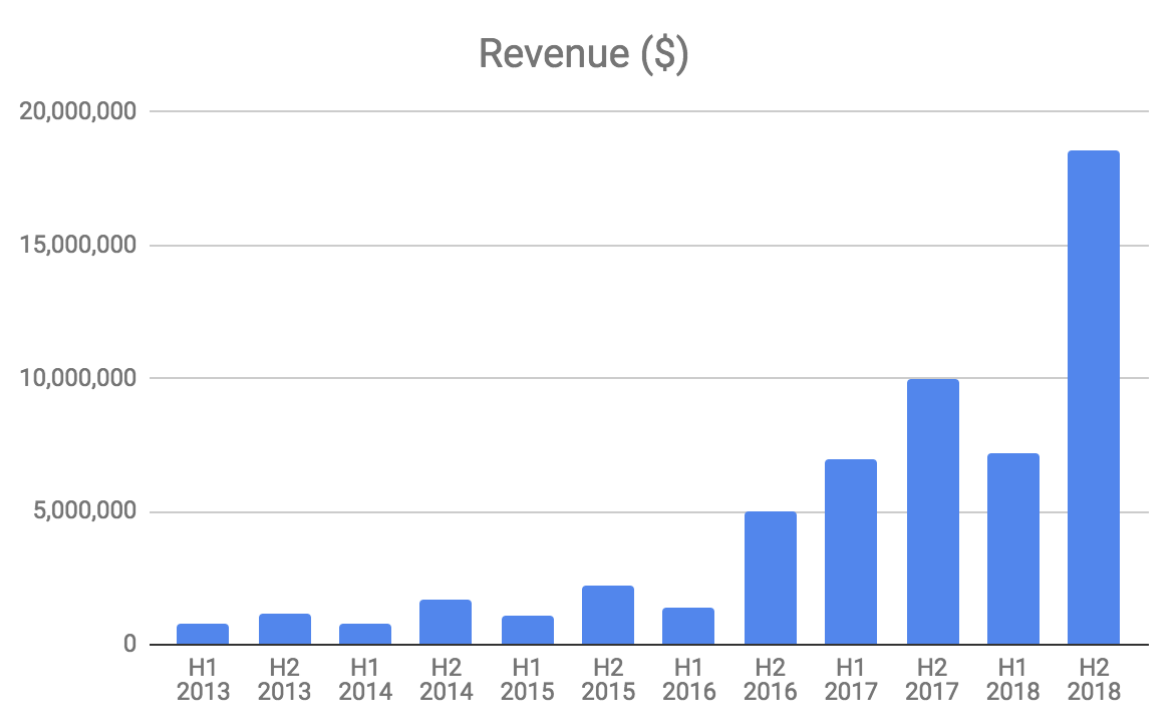

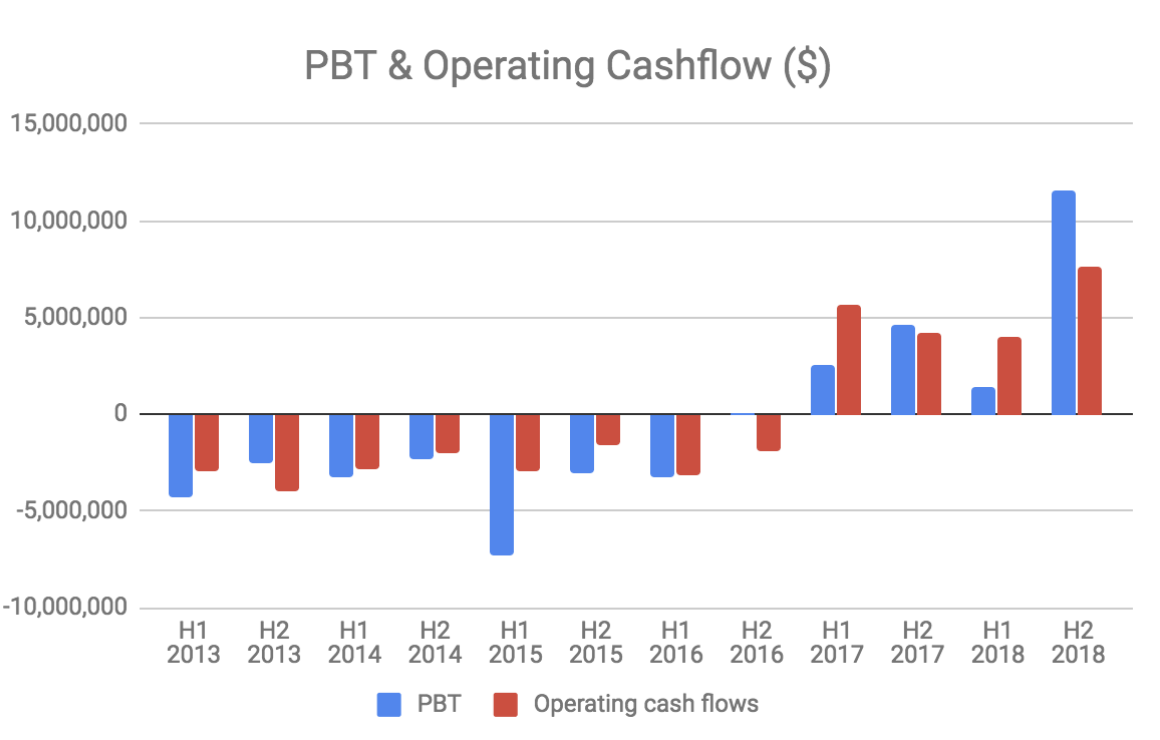

Clinuvel earns very high gross margins (>90%) and has a relatively low fixed cost base of about $10 million per year. The company has reached profitability and future revenue growth will largely fall to the bottom line.

Clinuvel has $36.2 million in cash and no debt.

The business is seasonal with revenue weaker in the first half of the year. This is because SCENESSE is primarily sold in the lead up to spring, summer and autumn in the Northern Hemisphere.

Clinuvel Executive Team

CEO Dr Philippe Wolgen was a promising soccer football player in his youth but instead chose to train as a craniofacial surgeon before becoming an equities analyst. Under his watch Clinuvel has regularly missed commercialisation and regulatory approval deadlines, but this is typical of early stage drug companies.

Clinuvel’s share price closed at $3.35 on 27 November 2005, the day before Dr Wolgen was appointed, and is now $18.34. He is jointly responsible for switching Clinuvel’s focus from developing a general use tanning agent to targeting rare genetic disorders, which has proven to be a successful strategy. He owns 5.4% of Clinuvel.

Chairman Stan McLiesh is the former general manager of pharmaceuticals at CSL Limited and joined the board in 2002.

Recently appointed non-exec director Dr Karen Agersborg is the daughter of former CSO Dr Helmer Agersborg, who passed away in 2012.

Board member Willem Blijdorp purchased $13.6 million worth of shares for $10 per share in July 2018.

Conclusion

Clinuval’s share price has risen sharply in recent months and is up more than more than 20% since I started researching this article. The company’s current market capitalisation of $880 million is reasonable given the potential of SCENESSE for treating EPP in Europe excluding the UK alone ($150 million to $600 million revenue opportunity). It is likely that US approval will follow, effectively doubling the company’s addressable market. Success with Vitiligo would more than double it again.

I intend to buy a small number of shares in the company, but not for at least two full trading days following the publication of this article. I think the key risk is the prospect of generic competition around ten years from now, but I would hope that the company has been successful in launching other products by then. Delayed safety issues are another risk, but given some patients have been taking the drug for more than a decade I think this risk is low, albeit potentially company destroying.

Note from Claude: I’d like to thank Matt for prioritising this work. This company looks promising to me, and I may buy some shares, after reflecting. However, I will wait at least two trading days to do so.

For exclusive content, join the Ethical Equities Newsletter.

Disclosure: Matt Brazier and Claude Walker do not own shares in Clinuvel at the time of publication. This article contains general investment advice only (under AFSL 501223). Authorised by Claude Walker.

Hi Matt, super article, great find, thanks for putting this together.

LinkFinally Clinuvel getting some attention. The potential is massiv and the stock is still a bargain, considering future growth potential, label extension, and its enorm profitability (72% free-cash-flow profitability in the last quarter). Is there any other pharma company with patient retention of 98% without even any sales force?

You could add the following clinical study on mice for the neuroprotective effects of Afamelanotide:

Mykicki, N., Herrmann, A. M., Schwab, N., Deenen, R., Sparwasser, T., Limmer, A., ... & Wiendl, H. (2016). Melanocortin-1 receptor activation is neuroprotective in mouse models of neuroinflammatory disease. Science translational medicine, 8(362), 362ra146-362ra146.

For the topical formulations brand names have been already registered: Chivére and Tsumoyl

Also there is first analyst coverage from Sphene Capital about Clinuvel:

Initial coveragy, January 2018: http://www.more-ir.de/d/16065.pdf

Update 25th June 2018: http://www.more-ir.de/d/16649.pdf

Update 7th September 2018: http://www.more-ir.de/d/16925.pdf

... in addition. Due to the EMA regulations, Clinuvel had to establish accredited expert centers where Scenesse is allowed to be administered from trained doctors. Along with this, Clinuvel had to establish a patient register to monitor the administration of Scenesse in EPP patients life-long and report yearly to the EMA. In my view this is also a huge competitive benefit. 1) Because Clinuvel captures a lot of data on Scenesse and 2) as it will be difficult for any generics to enter this market and be applied in the centers, when Clinuvel is responsible to capture patient data. Also those centres could be well used to treat other porphyria disease, when label extension is achieved. Waren Buffett would say it's a huge moat.

LinkHi Thomas,

LinkThanks for your comments and the links to those other reports, you clearly know Clinuvel well.

Is it possible that a generic could be approved with the same requirements to monitor and report to the EMA? Clearly, the regulatory burden is not so costly as to prevent Clinuvel from earning very high profit margins. Assuming a generic provider could get approval, why wouldn't it go to the same lengths as Clinuvel to take some of that fat margin?

The other risk that I failed to properly highlight in the original piece is reimbursement. What happens if other European countries besides the UK decide not to reimburse Scenesse?

Is it fair to use prevalence figures to measure the addressable market in the US when not everyone has access to health insurance?

Prevalence varies significantly by country and there is the risk that the estimates used above are not accurate.

Just trying to fully explore the risks to the investment case so forgive me if the above questions betray my ignorance.

Matt

Hi Matt

LinkThx for your comments and questions. You clearly have done your research :) Yes, I follow the company closely since many years. The Sphene Capital reports are really good and comprehensive.

My thoughts on your questions:

1) Generica: Sure, could be after patent expiration and the end of market exclusivity. EMA orphan market exclusivity for 10 years after approval and extention by another 2 years, if pediatric treatment is made available and approved (which Clinuvel is working on). Overall, most likely Cuv has exclusivity until 2026 in EU for EPP treatment. Due to the established monitoring requirements and patient register, I think it's just much more difficult for a Generica company to copy that or push Clinuvel out of the market. Also, if so, I don't think Clinuvel would be further responsible for monitoring, if the EMA accepted a generic to be applied in the centres. So how would this work, I don’t know. I assume, formally there could be generics, but practically I think it's more difficult to enter that market compared to a normal drug.. Also one might assume that prices per implant might drop over the coming 10 years, once a bigger patient population is treated. Also which company would take such efforts.. rather big pharma could buy out Clinuvel.

2) Reimbursement: With Germany and other key countries paying now (NL, DE, CH, ITA, AT, ES,...) a uniform price, I see a little risk that other countries will not follow. Germany is usually the reference market. UK is always a special case as they reimburse almost nothing (see cases of oncology treatments from Roche). Also, discussions with NICE are still ongoing (not yet finally "no").

3) Pricing: The treatment price is around 14'100 EUR per Implant (x4 = 56k, x6=84.6k) from my estimates. Currently 3-4 implants are administered and Clinuvel is trying to get 6 implants / year established.

4) Prevalence: Well yes, that's the only assumptions we have :) I would assume around 3000-4000 treatable EPP patients in the EU and around the same in the USA. In the EU core countries there are around 1200 registered patients (just those are around 100mn AUD revenues). Data from the national organization of rare diseases (USA) reported 4360 EPP patients. If we deduct kids and elderly I come to roughly 3000 patients in the USA. Also, as the treatment and awareness of EPP progresses there might be more and more patients being identified. I assume the penetration rate will increase over time.

5) Market potential: Broadly agree with your estimates. Just take a treated population of 3000 patients globally with FDA approval with just 3 implants and you will arrive at a market size of 200mn AUD as a quite low case. Apply a continuing net profitability on EPP with at least 50% (incl. taxes at some point) and we have 100mn AUD profits or over 2 EPS. Apply a P/E of x20-25 for a still growing company and the stock is worth 40-50 AUD just for a minimum EPP case. And here we didn't even talk about Vitiligo (blo

Thanks once again Thomas, these posts are a great addition to the original thesis. I agree that Clinuvel shares are good value at these prices, only wish I'd looked at the stock sooner!

Link