Beyond International has a long history of profitably producing niche television shows and effectively managing the copyright of those shows. The company also buys the rights to programs it doesn’t produce, and sells them into new markets. These activities account for most of Beyond’s profits, and I believe that this is where the company has a competitive advantage: a rare mix of knowledge, experience, networks and intellectual property. However, the company has four revenue streams.

TV production and copyright

- Produces programs commissioned by networks and buys the rights to externally produced television programs (or series). Manages the copyright of those programs. Ideally, that means selling the right to broadcast them.

Film and Television distribution

- Distributing Content (on behalf of producers).

Home entertainment

- Selling DVDs to the masses (and now also some digital sales).

Digital Marketing

- They call the four businesses BeyondD. Website creation, internet marketing, internet advertising businesses, and greatsites.com.au.

My Analysis of Beyond International

Because of the multiple revenue streams, I find Beyond International a difficult company to understand. However, looking at the company as a whole, it’s clear that in the last few years it has been the production and copyright segment that has grown earnings. While earnings from this core segment are not on a clear growth path, production and copyright reliably earns at least $2 million every half by my rough estimation. It’s not entirely accurate to consider the after tax earnings of this business in isolation from the other businesses, because all the business segments are interrelated, and obviously certain costs are shared between the businesses. However, for the sake of assigning a value to this segment, I’ve estimated the average after tax earnings per half to since 2007 to come in at over $3.2 million. I prefer to underestimate the value of a company than overestimate it. Notably, earnings from half to half seem to vary considerably, presumably depending on the success of individual programs. Hit shows such as Mythbusters and Selling Houses Australia clearly make a significant individual contribution to Beyond, over the years.

The earnings of the distribution business are pretty flat, perhaps growing slightly. The Home Entertainment division has been declining, which shouldn’t be a surprise to anyone, given that content is increasingly accessed over the internet. Management have not been caught flat-footed, however, and have begun digital sales, although they are currently not making a significant contribution to the bottom line. To me, this business is a “melting ice cube,” and it’s anyone’s guess as to how quickly it will melt. In the meantime, the company has recently purchased a suite of internet marketing businesses, which they have branded BeyondD. The jewel in that crown, I think, is First, a company that essentially designs, builds and maintains websites. This is a business with significant tailwinds, and while I am unable to assign it much value at the moment, if the management team is able to turn it around, that will be a serious boon to the company.

Readers should realise by now that much depends on management. Of key importance is to continue to buy and produce successful, profitable programs, on budget and on time. Additionally, shareholders must trust management to grow the new digital businesses, as they are not yet realising their potential, or justifying their purchase price. I’d be worried if management made another acquisition before bedding down BeyondD.

In light of the importance of management, I spoke to CEO Mikael Borglund recently. I began to realise how Beyond has grown over the years, and I couldn’t help suspecting that it is the networks and capabilities of the entire board that make this a quality company. Indeed, the board and management seem to have the right skills to guide the company. Directors’ interests are suitably aligned with shareholders and I believe that salaries are reasonable. As long as they focus on good customer relationships, and profitable operations, shareholders are likely to be rewarded in the long term. Between them, management and the board own almost 40% of the company. The chairman, Ian Ingram recently spent $2.3 million buying shares in Beyond at $1.26. I wonder when he'll have enough to be satisfied.

It’s probably worth noting that although Beyond earns a significant amount of revenue in $US, contracts are hedged, so in the short term, the company is not going to benefit from the falling Australian dollar. However, if the Australian dollar stays around 95c, shareholders can reasonably expect the impact will be immaterial. My understanding is that in the longer term, a lower Australian dollar should assist the company.

At any rate, the company is in fine health. At 31 December 2012, it had over $8 million in cash, and no bank debt. It has been paying a 3c per half, unfranked dividend. This is completely sustainable, although the company has signalled an intention to use cash for acquisitions, rather than to return it to shareholders. It’s impossible to say whether they might raise the dividend, but they could. In any event, a 6c dividend at a price of $1.50 represents a 4% yield, which isn’t too shabby.

I sold my shares in Beyond International very recently, because I have personal reasons for wanting cash. Also, because I conservatively value Beyond International at about $1.17 per share. The company is firmly on my radar because I believe it is a well-run business, with good economics, and a strong return on capital. I believe it has a reasonable edge, and, to put it simply, it satisfies most criteria on my investment checklist (especially if you consider successful TV series revenue to be somewhat like recurring revenue.) I look forward to reading the annual report. Readers should note that I have valued the BeyondD business at about $300,000, as I am not assuming growth at this stage. This is the likely flaw in my valuation, and should I be proved wrong, the share price will probably move well beyond $1.50. Ha! Trading at under PE 10, I'd say the shares are close to fair value. If they are again offered for a discount, I might grab some.

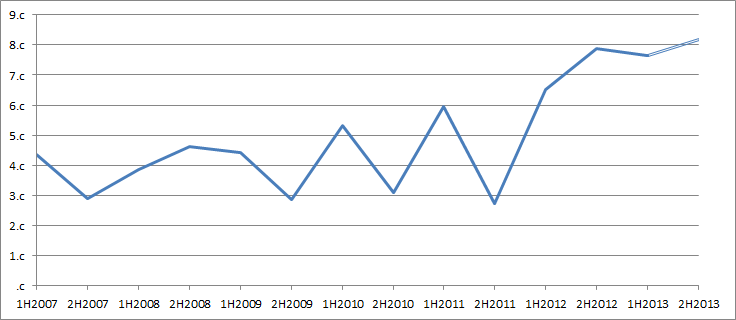

Historic and Forecast Earnings Per Share for Beyond International

The forecast EPS is based on 10% growth for the full year (the low end of guidance)

The forecast EPS is based on 10% growth for the full year (the low end of guidance)The Author does not have a direct interest in shares of Beyond International. The Author is not aware of any indirect interest in BYI.

Want to hear about it if BYI shares drop to a great price? Sign up to the newsletter for free!